There are three Lifestyle Profiles to choose from.

The PSPS Multi-asset Lifestyle Profile

The Trustee has designed this profile as a ‘whole of working life’ ready-made strategy for those members who wish no involvement in choosing their investment strategy.

If you have not decided how to invest your Personal Account, it will be invested using this Lifestyle Profile.

Like the alternative Lifestyle Profiles available to you, the PSPS Multi-asset Lifestyle profile initially invests in higher risk funds, gradually transitioning to lower risk funds as you approach your Selected Retirement Age.

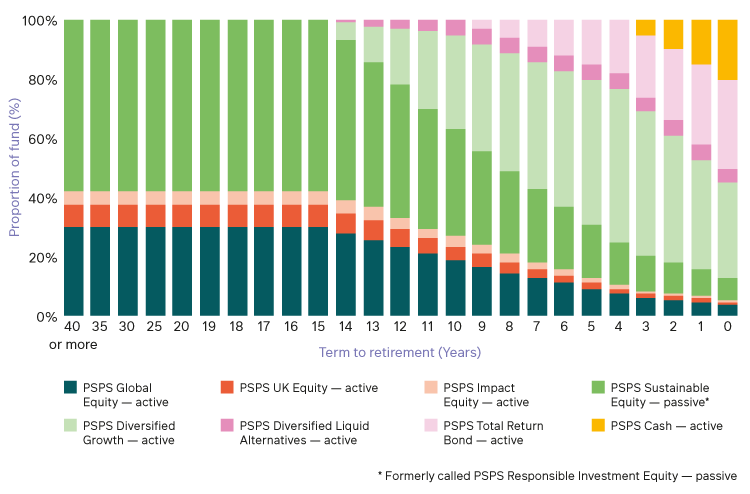

Aims: To target higher returns whilst members are far from retirement by investing in equities and then progressively switching into a lower risk, more diversified portfolio. From 15 years to retirement, there is a gradual switch into a more cautious diversified investment strategy so that when members are within one year of their Selected Retirement Age, the majority of assets are held in lower risk funds.

Overview: The Lifestyle Profile invests 100% in equities up to 15 years from retirement followed by a gradual switch into the PSPS Diversified Growth — active fund and the PSPS Diversified Liquid Alternatives - active fund. From 10 years to retirement, there is a gradual switch of a proportion of the strategy into PSPS Total Return Bond Fund and then the PSPS Cash — active fund.

Suitable for:

Members who are further away from retirement seeking exposure to higher returning investments initially and less investment risk as their term to retirement reduces; or

Members closer to retirement who do not know how they will take their benefits and those who expect to take their benefits in the form of a tax-free lump sum or switch to another registered pension scheme offering income drawdown.

For more information see the Investment Guide in the Document library.

The two targeted alternative Lifestyle Profiles are explained below.

Targeted Alternative Lifestyle Profiles.

We’ve created two variations of the Multi-asset Lifestyle Profile; for those members who know how they plan to use their Personal Account at retirement and want a ready-made investment strategy.

PSPS Annuity at Retirement Lifestyle

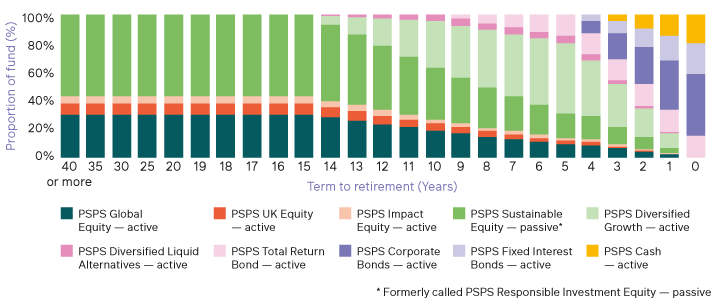

Aims: To target higher returns whilst members are far from retirement by investing in equities and then progressively switching into a lower risk, more diversified portfolio. From 15 years to retirement, there is a gradual switch into a more cautious diversified investment strategy, targeting Annuity, so that when members are within one year of their SRA, the majority of assets are held in lower risk funds.

Overview: The Lifestyle Profile invests 100% in equities up to 15 years from retirement followed by a gradual switch into the PSPS Diversified Growth — active fund and Diversified Liquid Alternatives — active fund. From 10 years to retirement, there is a gradual switch to a proportion of the strategy into PSPS Total Return Bond — active, PSPS Corporate Bonds— active, PSPS Fixed Interest Bonds — active and then the PSPS Cash — active fund.

Suitable for:

• Members who are further away from retirement seeking exposure to higher returning investments initially and less investment risk as their term to retirement reduces; or

• Members closer to retirement who expect to use their Personal Account to buy an annuity policy (or similar) to provide a regular fixed income in retirement.

For more information see the Investment Guide in the Document library.

PSPS Cash at Retirement Lifestyle

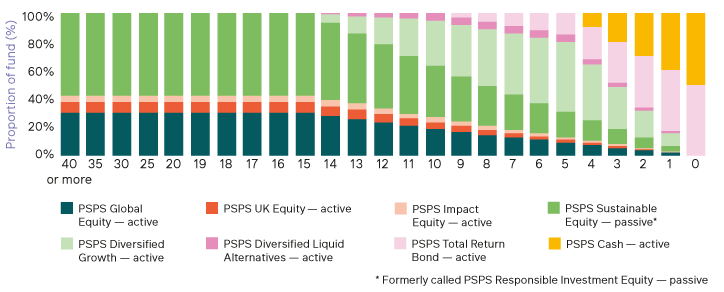

Aims: To target higher returns whilst members are far from retirement by investing in equities and then progressively switching into a lower risk, more diversified portfolio. From 15 years to retirement, there is a gradual switch into a more cautious diversified investment strategy, targeting cash withdrawal, so that when members are within one year of their SRA, the majority of assets are held in lower risk funds.

Overview: The Lifestyle Profile invests 100% in equities up to 40 years from retirement followed by a gradual switch into the PSPS Diversified Growth — active fund. From 10 years to retirement, there is a gradual switch to a proportion of the strategy into PSPS Total Return Bond — active, and then the PSPS Cash — active fund.

Suitable for: • Members who are further away from retirement seeking exposure to higher returning investments initially and less investment risk as their term to retirement reduces; or • Members closer to retirement who expect to use their Personal Account to fund one or more cash sums at retirement.

X

DISCLAIMER: The purpose of this video presentation is not to provide tax or financial advice. The Trustee of the Prudential Staff Pension Scheme is legally prevented from giving financial advice. This video presentation aims to help you better understand certain aspects of your pension scheme and the choices you may have. All benefits from the Prudential Staff Pension Scheme are payable in accordance with the Trust Deed and Rules, the legal document governing the Scheme. In the unlikely event of any discrepancy between any information provided to you in this presentation and the Trust Deed and Rules, the Trust Deed and Rules will prevail. Viewing the online learning modules remotely through Citrix Access Gateway may affect the video quality. You may avoid this by viewing them directly from the Internet.